Life Insurance 101: How to Know If You Need It

Nearly one in every four Americans rely on the Social Security program. For a system as far-reaching and critical as this one, it’s no wonder the topic is always making headlines, and even has an entire month designated to it. To “celebrate” National Social Security Month, the Social Security Trust Fund’s Board of Trustees releases their annual report detailing, among many other things, its long-term solvency.

You may have seen a few sensational headlines exploiting the often misunderstood terms “bankrupt” and “insolvent” associated with the trust fund’s long-term outlook. Given the importance of Social Security in most retirement plans, it's no surprise attention is drawn to its long-term sustainability. Because of this constant drumbeat of Social Security “running out,” it is also an incredibly common concern we hear from our clients, both young and old alike.

To address these concerns, we hope to shed some light on how the program works, why we are confident it will be around for a long time to come, though likely not in its current form, and how we help clients understand their options when it comes time to file for their own benefits.

How Social Security Works

Turning eighty-nine years old this August, the Old-Age, Survivors, and Disability Insurance (OASDI) program, commonly referred to as Social Security, was designed to supplement retirement income, acting as a form of insurance by ensuring our population’s most vulnerable could meet their most basic needs. When it comes to retirement savings, the unfortunate reality is that around half of retirees have less than $1,000 saved in retirement accounts.1 Despite criticisms over the years, Social Security serves as a crucial social safety net. Its existence prevents millions from facing the risk of starvation and homelessness – a trade-off many are willing to accept.

If you have ever spent a few minutes reviewing your paycheck, you are likely familiar with the FICA tax. Created by the Federal Insurance Contribution Act, this tax is composed of Social Security (OASDI) and Medicare payroll taxes. Whether you earn income working for yourself or someone else, you are expected to withhold the following amounts on each dollar:

| FICA Tax | Employees | Employers | 2024 Wage Limit |

| Social Security (OASDI) | 6.2% | 6.2% | Up to $168,600 |

| Medicare | 1.45% | 1.45% | N/A |

| Additional Medicare Tax | 0.9% | N/A | Over $250,000 (Joint) & $200,000 (Single) |

It is also worth noting you pay FICA taxes before most deductions come out of your paycheck, unlike Federal and state income taxes. For example, HSA contributions (deducted directly from your paycheck), certain SEP IRA contributions, and payments for health and dental insurance are deducted before FICA taxes. This is also why the amounts in boxes 3 and 5 on your IRS Form W2 are almost always greater than box 1.

The Current Trust Fund Surplus

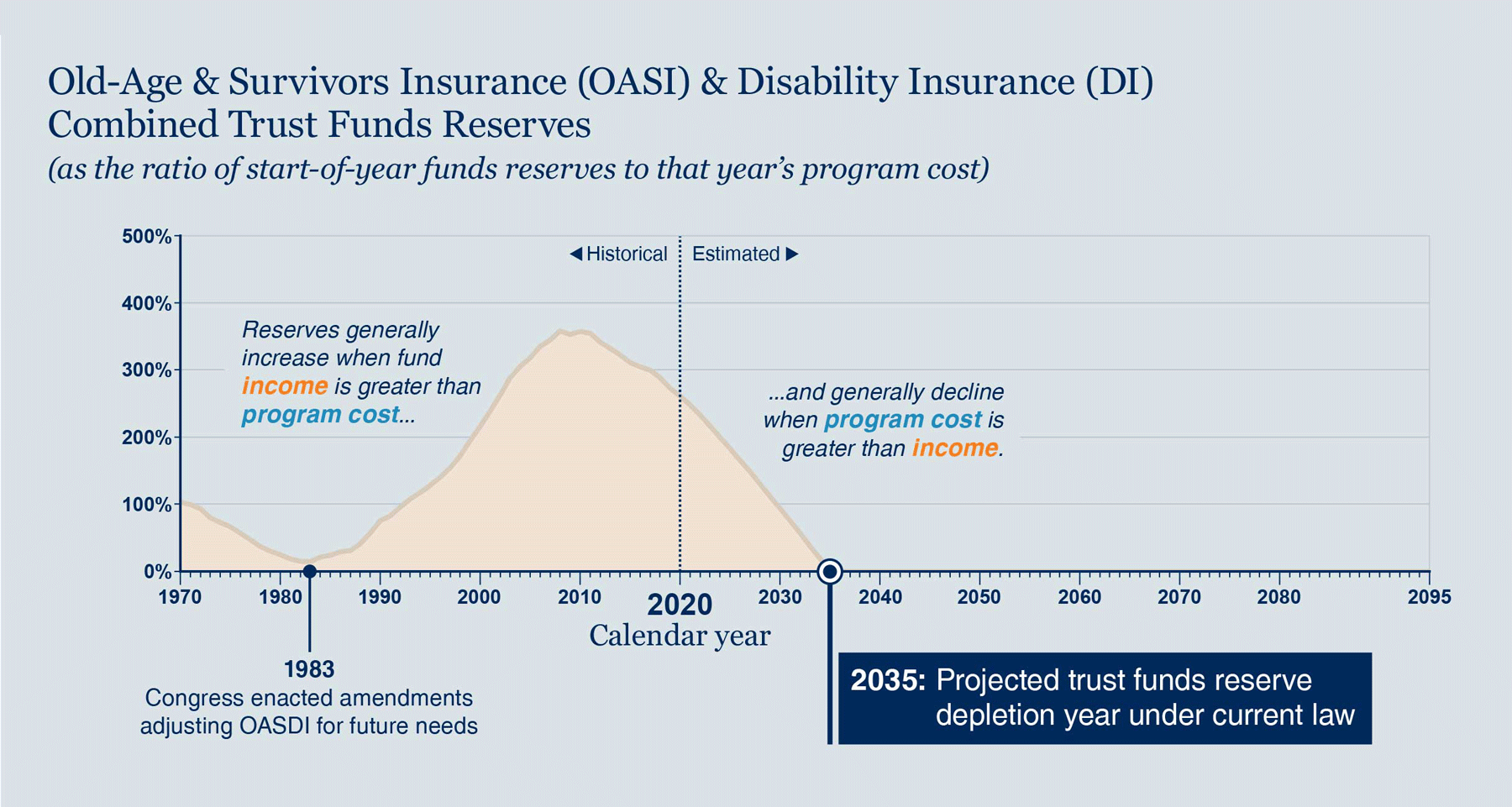

The program was designed as a pay-as-you-go system, meaning ongoing contributions are used to pay current benefits. In 1983, with only a few months until disaster and insolvency (i.e., incoming contributions would not cover 100% of benefits owed), a Democratic House and Republican Senate and President worked together to raise payroll taxes and increase Full Retirement Age from 65 to 67.

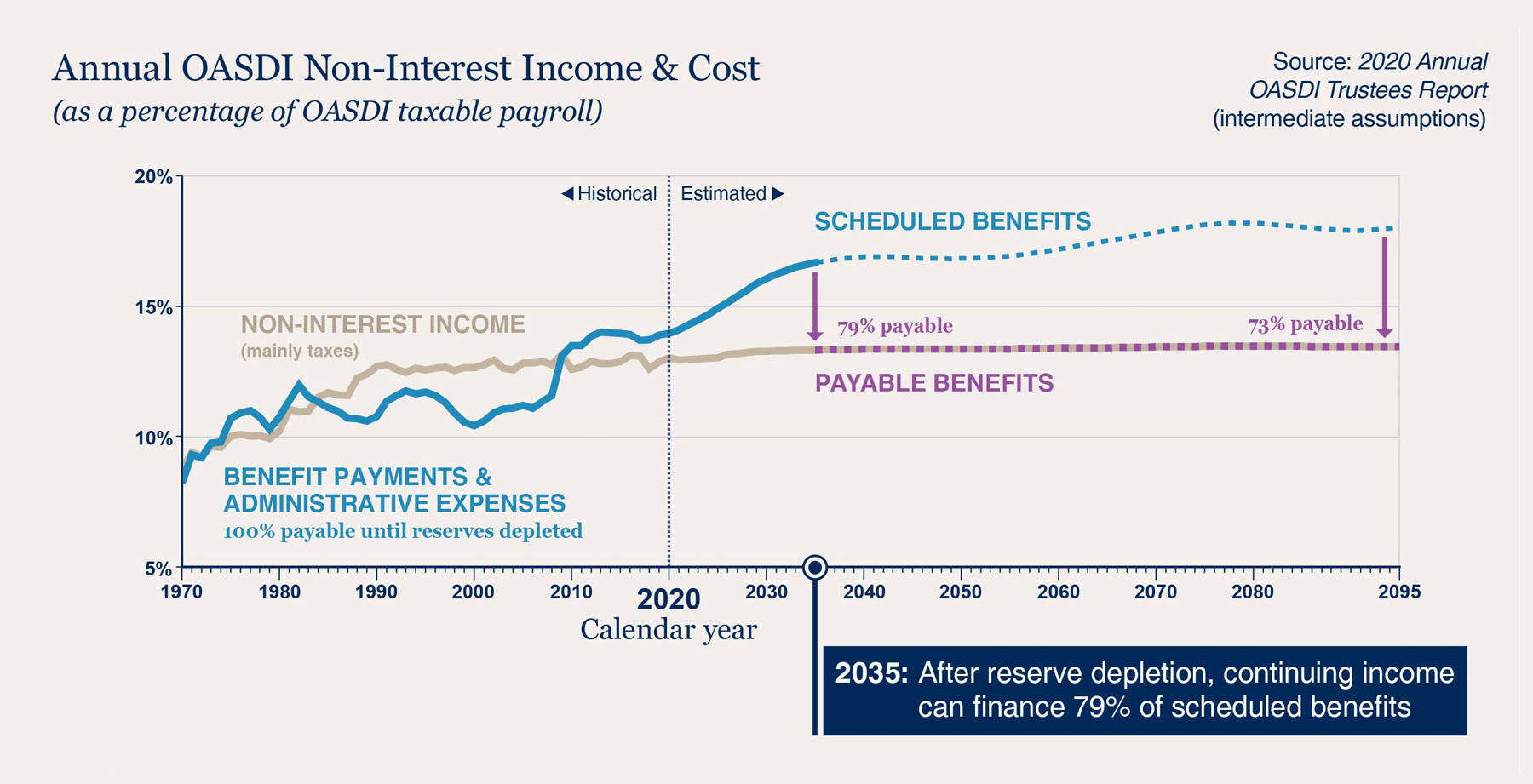

Acting with prudent foresight and recognizing the demographic challenges resulting from the baby boomer generation, Congress knew they had to build up the trust fund’s “rainy day funds” and generate a surplus for the next few decades to weather the eventual income shortfall due to a high ratio of retirees relying upon the system. After the surplus is depleted in 2035, the program anticipates being able to pay only 83% of currently scheduled benefits, with this dropping further to 73% by 2098.

Source: 2020 Annual OASDI Trustees Report (SSA.gov/OACT/TR/)

Potential Remedies

For those familiar with Social Security and how it works, the potential solutions for fixing it are well-known and relatively straightforward. The biggest challenge is finding compromise in Washington that does not disproportionally disadvantage one group over another – an almost impossible task.

Ultimately, it will likely take a combination of the following to provide comprehensive reform to stave off the projected Social Security shortfall. Similar to how the Full Retirement Age was raised from 65 to 67 over many years, the changes will likely be implemented very gradually over many years.

The Committee for a Responsible Federal Budget has designed a helpful calculator that quantifies, as a percentage, the potential reduction in the projected shortfall based on the following solutions:

- Increase payroll taxes. There are two ways this can be accomplished: by increasing or eliminating the current wage cap of $168,600 or raising the current tax rate of 6.2% for both employees and employers. Eliminating the wage cap could close the shortfall by an estimated 60% and raising the payroll tax by 3.5% total (1.75% split between employee and employer) could eliminate the shortfall altogether.

- Increase Full Retirement Age. Advances in medicine and health care, along with a focus on healthier lifestyles, have modestly improved life expectancies since the start of the program in 1935. Retirement is lasting longer than it used to, adding further strain to the system. In 2015, there were about three workers paying into the system for each beneficiary and it’s expected to drop to around two workers in 2035. For every year Full Retirement Age is increased, the shortfall is reduced by around 13%.

- Expand trust fund investment options. By law, the Social Security trust fund surplus can only be invested in securities guaranteed by the Federal government. Historically, stocks and other types of bonds have outperformed Treasuries, though with increased volatility. It is estimated that investing a portion of the trust fund surplus would close the shortfall by around 5%. However, it becomes a bit of a catch-22: if there isn’t a trust fund surplus to begin with, there isn’t an opportunity to invest those assets for the long term. And, as we know from investment management 101, the longer your time horizon, the more volatility your portfolio can sustain. If you are paying out benefits as soon as you receive the revenue, the time horizon is non-existent.

- Means-testing. Many are surprised to learn Social Security benefits are already means-tested when you are paying into the system. To put it simply, the first $12,000 or so dollars you earn each year is credited or rewarded a much higher percentage (i.e., 90%) of benefits than your next $60,000 earned and beyond (32% and 15%, respectively). As a result, means-testing on the way out is often a nonstarter for most, but phasing out benefits for the top 1% of earners could reduce the shortfall by around 17%.

- Cost-of-Living Adjustments. Thousands of inflation numbers are published each month by the Bureau of Labor Statistics, but the headline-grabbing number is the CPI-U, or the Consumer Price Index for All Urban Consumers. While CPI-U gets the most attention, Social Security cost-of-living adjustments, or COLAs, are actually tied to the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) to reflect recipients’ inflation experience more accurately. Just the same, neither index accounts for an individual’s natural tendency to substitute an expensive product with a cheaper one. The “chained” CPI-W accounts for this substitution effect and, as a result, tends to increase more slowly than CPI-W, but is also considered more realistic. Indexing Social Security to “chained” CPI-W instead of the current “unchained” CPI-W could close the shortfall by an estimated 18%.

A wise man once said, “reality is messier than theory.” In other words, when it comes to fixing Social Security, it is easier said than done, but we believe we have the tools, and motivation, to fix it. That being said, the situation is only growing more critical with time – the sooner changes can be made to the program, the more modest the adjustments can be.

How to Prepare

Deciding when to take Social Security is an important part of your financial journey, but many are unsure when that right time is. You may have heard the saying, “I’ll tell you exactly when to file for Social Security, if you can tell me when you’ll pass.” Like many parts of financial planning, it is a decision based on probabilities and personal life expectancy.

The optimal claiming strategy varies based on an individual's financial situation and cash flow needs. Because everyone’s situation is unique, we often recommend clients provide a copy of their most recent Social Security statement, which can be accessed on ssa.gov. Using accurate data and looking at it from many different angles helps our clients visualize their wealth over time based on filing at different ages. For example, an individual in poor health would greatly benefit from claiming it early, whereas someone in excellent health, with a robust family history, might find it advantageous to delay.

Source: 2020 Annual OASDI Trustees Report (SSA.gov/OACT/TR/)

For younger clients, the future of the Social Security program is slightly more uncertain, though we can start with the projected payable benefits as a baseline if no changes are made. A practical approach we often use is to assume a conservative Social Security benefit, perhaps 75% of the current promised benefit, and then look for opportunities to compensate for it in other parts of the plan, such as increased savings or slightly lower spending goals.

While the future of Social Security might be out of our hands, we hold significant control over how much we save and budget for our retirement years.

Sources: Federal Reserve’s 2022 Survey of Consumer Finances, Social Security Trust Fund’s Board of Trustees Annual Report

Please consult with an attorney or a tax or financial advisor regarding your specific legal, tax, estate planning, or financial situation. The information in this article is not intended as legal or tax advice.