Webinar for Individuals & Families: 2026 Mid-Year Outlook

Key Takeaways

1. Tax preparation is often an exercise in looking back but as long-term planners, we are also looking at what’s on the horizon.2. Many changes to individual income taxes in the Tax Cuts and Jobs Act of 2017 are scheduled to ‘sunset’ at the end of 2025 unless additional congressional action is taken.

3. 2026 will be here before we know it. While tax rates may be at historically low levels, there are tax strategies to consider with your financial consultant to smooth out and reduce your taxes over the long-term.

Everyone enjoys a nice sunset, however, the upcoming ‘sunset’ of the Tax Cuts and Jobs Act (TCJA) provisions at the end of 2025 is not something most taxpayers are looking forward to. And while most people tend to look back when it comes to taxes, we as planners prefer to look out over the long-term, seeking to minimize and smooth taxes over many years. For this reason, it’s prudent to start thinking about how your taxes might change in 2026, especially since any major changes in the legislation framework or extension of the TCJA provisions are unknown at this time with the upcoming presidential election. If no action is taken, the act will sunset automatically.

The following is a list of the most notable tax changes and potential planning opportunities to consider as you meet with your financial advisor, tax professional, and estate attorney from now until 2026.

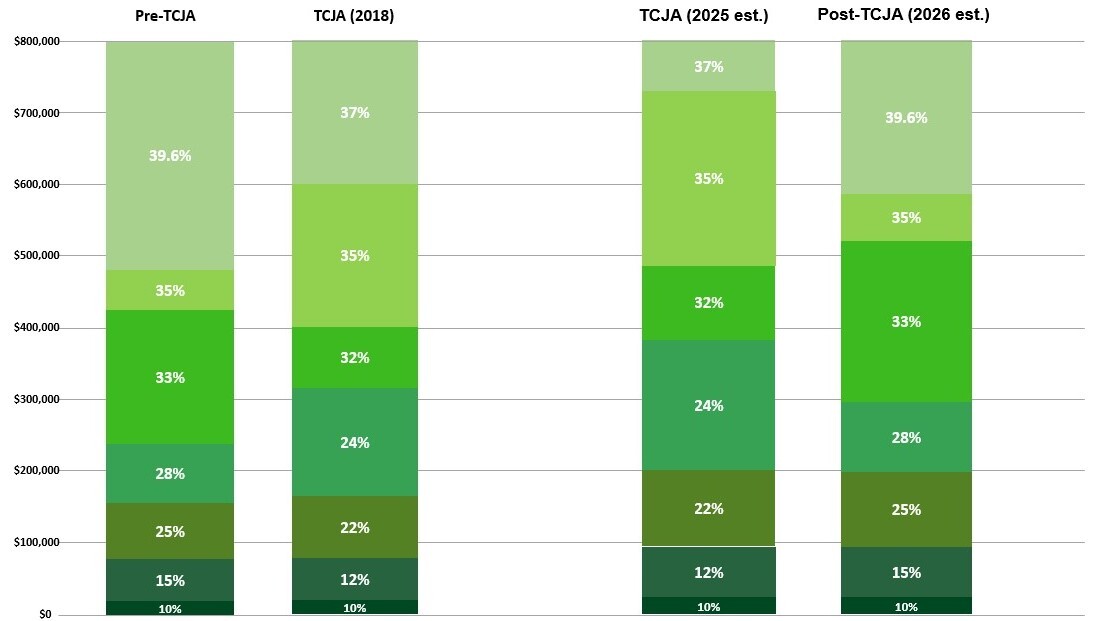

Income Tax Brackets

The one change likely felt by all taxpayers was the lowering of the marginal tax rates and the expansion of the tax brackets. Not only did the brackets get larger, but the following marginal tax rates were reduced:

- 39.6% to 37%,

- 28% to 24%,

- 25% to 22%,

- and 15% to 12%.

Below is a visual of how much they changed in 2018 for Married Filing Jointly filers and our estimate for their reversion in 2026.

Married Filing Jointly Tax Brackets Throughout the Years

For illustrative purposes only.

The TCJA also ‘detached’ the long-term capital gains (LTCG) tax bracket from the income tax bracket. With the upcoming sunset, the long-term capital gains tax brackets will once again be tied to the newly compressed income tax brackets like so:

- 0% LTCG tax rate for those in 10% and 15% ordinary income tax bracket

- 15% LTCG tax rate for those in 25%, 28%, 33%, and 35% ordinary income tax bracket

- 20% LTCG tax rate for those in 39.6% ordinary income tax bracket

Planning Opportunity: Given these historically low tax rates, consider using the next three years to explore partial Roth conversions, accelerate income and realize capital gains while it’s advantageous to do so.

Estate & Gift Tax Exemption

The TCJA doubled the per person Federal estate and gift tax exemption and is set to revert, when adjusted for inflation, to somewhere around $7 million per person beginning in 2026. The IRS has also issued regulations stating that lifetime gifts more than the future lower exemption amount will not be subject to ‘claw back’. In other words, this temporary increase is a one-time ‘use-it-or-lose-it’ bonus unless further Congressional action is taken to extend it.

Planning Opportunity: Those with sizable estates (greater than $40 million) should consider making substantial gifts before the change. Those with smaller estates (i.e., $10m - $20m) should explore estate planning techniques such as annual gifting or techniques that remove assets from your estate while still providing access like Spousal Lifetime Access Trusts (i.e., SLATs).

Standard Deduction & Personal Exemptions

The TCJA eliminated the personal exemption ($4,050) and doubled standard deductions, which are adjusted for inflation each year. The standard deduction for single filers went from $6,350 to $12,000 and married filing jointly increased from $12,700 to $24,000. It was estimated that these changes resulted in a 20% reduction in taxpayers who used itemized deductions. After the standard deduction peaks in 2025 and is reduced by half in 2026, itemizing will become much more appealing for many.

Planning Opportunity: Take advantage of the increased standard deduction for the next three years by ‘bunching’ charitable contributions or other deductions. This allows you to potentially take a large, itemized deduction in one year and take the standard deduction the other two years. Since the TCJA also limited the State and Local Income Tax deduction to $10,000 and is expected to sunset as well, consider paying these taxes on or after January 1, 2026, if you are planning to itemize.

Section 199A Qualified Business Income

One of the most substantial changes under the TCJA was the Section 199A Qualified Business Income Deduction that allowed for a tax deduction of up to 20% of business income for sole proprietors, LLCs, partnerships, S Corps, trusts, and estates. The main reason for this deduction was to match a rather large (and permanent) C-Corp tax rate reduction also put into place under the TCJA. Taxpayers with an AGI below $170,050 (single) and $340,100 (married) qualify for the full 20% deduction with a complete phase out at $220,050 and $440,100 respectively.

Planning Opportunity: Taxpayers utilizing the 199A deduction should identify ways to maximize this deduction over the next three years while also considering different entity structures (S Corp, C Corp, partnership, LLC, etc.) to determine the most tax-efficient framework once it sunsets.

Alternative Minimum Tax

Alternative Minimum Tax, or AMT, also received a major makeover under the TCJA. AMT is a provision for high earners requiring them to calculate their taxes two ways, using traditional income tax and AMT rules then paying the higher of the two tax liabilities. The AMT exemption increased under TCJA from $54,300 to $70,300 for individuals and $84,500 to $109,400 for married couples. More substantially, the income exemption phase out was increased from $120,700 to $500,000 for individuals and $160,900 to $1,000,000 for married couples. These changes reduced the amount of AMT taxpayers from 5 million to only 200,000.

Planning Opportunity: For those previously subjected to AMT, they are likely painfully aware of what can trigger this parallel tax system. Therefore, those with incentive stock options, private activity bond interest, foreign tax credits, passive income and losses, and net operating loss deductions will want to minimize these once the sun has set on these generous AMT provisions in 2026.

Sunsets are great – but paying less in taxes is even better.

Finding the right balance is key to long-term tax planning. We help our clients plan based on the current tax rules but also want to position them for many potential tax environments. Sometimes paying a bit more in taxes now can avoid much larger tax liabilities down the road. Just because something minimizes taxes this year doesn’t mean it will minimize your total lifetime taxes. In other words, don’t let the ‘tax tail wag the dog’ when it comes to tax planning.

Source: Congress.gov

Please consult with an attorney or a tax or financial advisor regarding your specific legal, tax, estate planning, or financial situation. The information in this article is not intended as legal or tax advice.