.jpg?width=500&height=500&name=iStock-512986393%20(1).jpg)

5 Ways Families are Rethinking Wealth Transfer

In this final part of our ‘How to Create an Endowment Spending Policy’ series, we’re going to simulate how different rules have behaved using historical market data. To recap, In parts I and II, you gained insight on guidelines for how to set a good policy and the definitions of different spending rules, respectively.

When looking at behavior of the different spending rules, let's consider a hypothetical endowment with a portfolio value of $1 million. For this illustration, we'll use two prior periods in the market’s history: (1) the decade of the 1970s, generally characterized by high inflation, low economic output (i.e., stagflation), and volatile market returns for both stocks and bonds; and (2) the decade of the 2010s, a period of recovery from the great recession, with low inflation, gradually falling unemployment, low economic growth, and low volatility in investment markets. Other assumptions include:

- A 5% spending rate for each of the spending rules, where applicable.

- Portfolio returns are based on index data weighted 70% to large cap stocks and 30% to intermediate-term treasury bonds. This is meant to represent a typical permanently endowed portfolio. Inflation is represented by the Consumer Price Index.

- The Simple Market Value rule applies the spending rate to the beginning market value of each year.

- The Average Market Value rule uses a 3-year calendar year average value based on each year’s beginning value.

- The Inflation-Adjusted rule has initial spending of 5%, then adjusts each year’s subsequent spending by the inflation rate.

- The Hybrid rule takes 50% of what spending would be under the Average Market Value rule, and 50% of what spending would be under the Inflation-Adjusted rule.

- All market values are depicted as “Real” values, meaning they are adjusted for the impact of inflation since the beginning of each simulation.

- No taxes or investment costs are assumed.

How did each of these spending rules perform during these contrasting time periods?

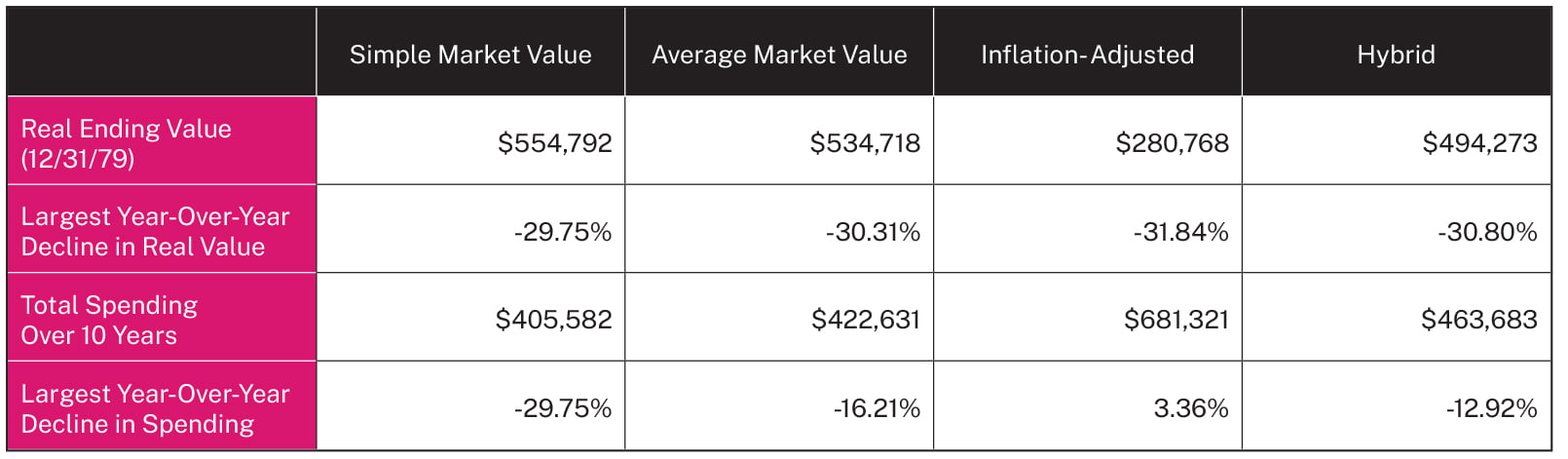

1970 to 1979

Annualized Nominal Investment Return: 6.56%

Annualized Inflation: 7.37%

The 1970s were a difficult time for investors, as the combination of middling returns and high inflation resulted in negative real returns, even before any spending is factored in. Each of the four spending rules saw a fall in market value. However, the difference between the Inflation-Adjusted rule and the Simple Market Value and Average Market Value rules is meaningful. Spending under the Inflation-Adjusted rule never fell year-over-year, despite a meaningful market drawdown in 1973, meaning that the portfolio spent more than the other rules, but left less invested. Spending under the Average Market Value Rule was steadier compared to the Simple Market Value Rule, but still more variable compared to the Inflation-Adjusted or Hybrid rules.

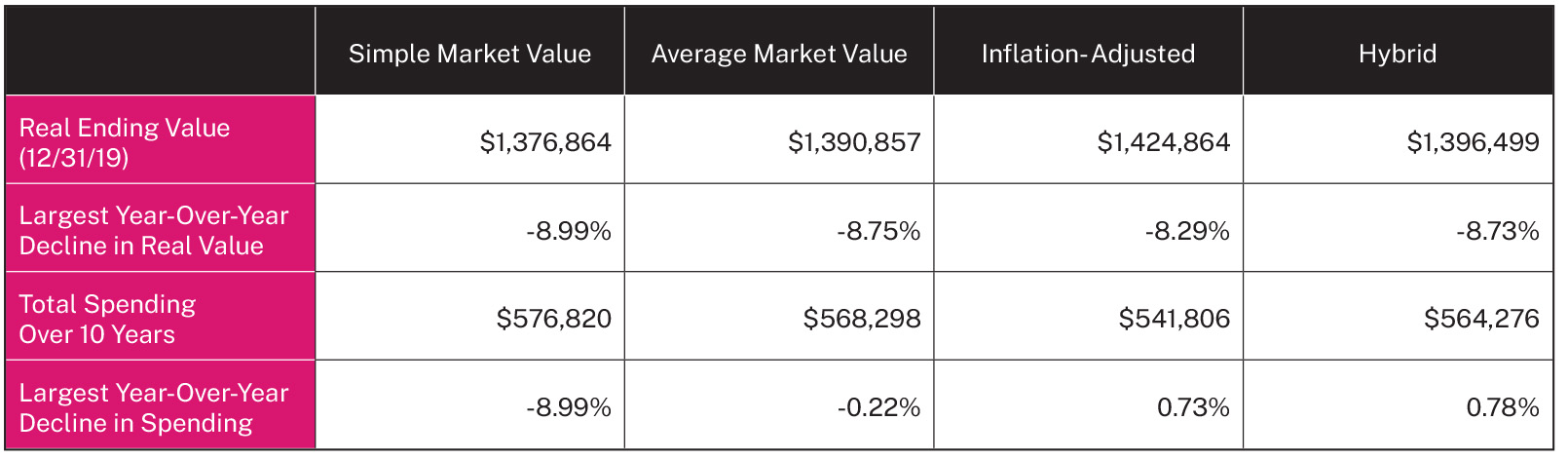

2010 to 2019

Annualized Nominal Investment Return: 10.59%

Annualized Inflation: 1.75%

The stock market drove good returns for investors in our hypothetical 70%/30% portfolio. Inflation was also relatively low, resulting in real growth exceeding 8%. Hence, each of the spending rules saw inflation adjusted growth in the decade. The Inflation Adjusted rule slightly outpaced the others in real ending value, but also had the lowest amount spent, since spending is tied directly to inflation. Despite seeing the largest decline in year-over-year spending, the Simple Market Value rule also enabled the most spending overall as spending is more closely tied to the portfolios current market value under this approach.

Conclusion

There is no one size fits all to endowment spending policies. These time periods were chosen to represent two extremes in the market environment. Non-profit investors would do well to enact a policy that will meet their expectations in a variety of environments while understanding the natural tradeoff between predictable, consistent spending, and a portfolio’s capacity to grow assets.

Our hope is that this series on spending policies can provide guidance for organizations on how to craft their own policy. In Part I , we outlined important questions and best practices. In Part II , we defined different spending rules. In Part III, we tested each of these rules to provide historical context for decision-makers. Organizations can conduct their own simulations using their own sets of assumptions and arrive at a policy that best meets their individual needs.

Helping organizations like yours create a spending policy that is tailored to your specific needs is just one of the ways we can help you succeed. Schedule a call with us today to learn more.

Your roadmap to growing your endowment

If you’re looking for ways to effectively grow your organization’s endowment, our toolkit can help you get there! Featuring multiple donor outreach templates, an endowed giving prospect scorecard, infographics, and more, this toolkit is filled with actionable resources to help enhance your fundraising.

Source: Morningstar, Analysis: Manning & Napier.

Morningstar, Inc. is a global investment research firm providing data, information, and analysis of stocks and mutual funds. ©2023 Morningstar, Inc. All rights reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied, adapted or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information, except where such damages or losses cannot be limited or excluded by law in your jurisdiction. Past financial performance is no guarantee of future results. The information in this paper is not intended as legal or tax advice. Consult with an attorney or a tax or financial advisor regarding your specific legal, tax, estate planning, or financial situation.