Webinar for Individuals & Families: 2026 Mid-Year Outlook

Families can now register for a Trump Account in advance of their official launch date of July 4, 2026. Accounts set up on behalf of qualifying children will also receive a $1,000 seed contribution from the federal government.

Here is what you need to know, and how we think about them.

What are Trump Accounts?

Introduced with the One Big Beautiful Bill Act of 2025 and called a Section 530A account – more commonly known as a "Trump Account” – is a new savings vehicle for kids and can be thought of as a “starter” retirement account for kids to maximize compound growth.

In many ways, a Trump Account is structured as a traditional Individual Retirement Account (IRA) for children under 18. It is owned by the child but managed by a parent or guardian until the child turns 18. At that point, the account converts to a standard traditional IRA with the normal IRA rules applying from then on.

During childhood, the money grows tax-deferred and cannot be withdrawn. Investments are restricted to low-cost US index funds designed to maximize long-term growth while minimizing risk. At 18, the child gains access to these funds, but the same early withdrawal penalty applies to these accounts, similar to IRAs. However, there are a few carveouts that allow for flexibility, including qualified education expenses, first-time home purchases (up to $10,000), and birth or adoption expenses (up to $5,000). The funds accumulated during the growth period can provide a meaningful starting point for future goals such as retirement, purchasing a home, or pursuing additional education.

Who Can Contribute & How

Contributions come from four sources, each with different rules:

The federal government establishes these accounts with Robinhood or The Bank of New York Mellon Corporation (BNY) after receiving an application and makes a one-time $1,000 seed contribution for children born between January 1, 2025 and December 31, 2028.

Family can collectively contribute up to $5,000 per child per year. Unlike a standard IRA, the child isn’t required to have earned income. The family can also transfer the Trump Account from Robinhood directly to a new Trump Account for the same child set up elsewhere.

Employers can contribute up to $2,500 per year on behalf of an employee's eligible child through a formal Trump Account Contribution Program. These contributions are excluded from the employee's taxable income. Note that the $2,500 cap applies across all of an employee's children combined, not per child. Any employer contributions also count towards the $5,000 per child per year contribution limit.

Qualifying governments and non-profits may also contribute outside the standard limits in certain circumstances. These will be broad based contributions and must specify a “qualified class” of account beneficiaries.

$5,000 |

2025–2028 |

Age 18 |

| Max annual contribution by family and employers | Kids born from 1/1/25–12/31/28 are eligible for the $1,000 seed contribution | Age when the account converts to a traditional IRA; child takes ownership |

To open an account, submit Form 4547 through IRS.gov, download the associated app, and then wait for the invitation to open the account. These details and others can be found at TrumpAccounts.gov.

When Opening a Trump Account Makes Sense

These accounts are worth paying attention to, but not every feature is right for every family. We believe in the power of compounding and so capturing the $1,000 seed contribution is a no-brainer, but committing your own dollars requires a real conversation first. Here is how we think about it.

Reasons for Opening:

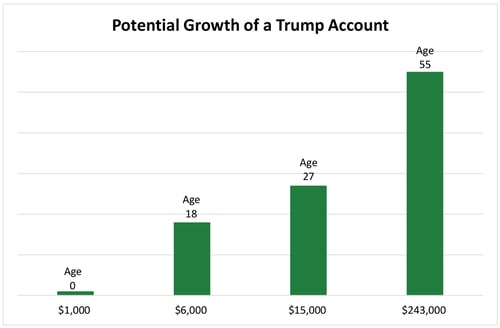

- A child is born between 2025 and 2028

Open an account and claim the $1,000 government seed. It has potentially 18 years to compound in a tax-deferred account. There is no good reason to skip it. An account with just the initial $1,000 could grow to:

For illustrative purposes only.

Source: trumpaccounts.gov

- Employer offers contributions

An opportunity to capture tax-free money for your child's future at no cost to you is a straightforward benefit to take.

Reasons for Caution:

- Gift tax issue

Unlike 529 plan contributions, your personal contributions to a Trump Account may not qualify for the annual gift tax exclusion ($19,000 per person in 2026). That means each dollar contributed could technically count against your lifetime estate and gift tax exemption ($15 million per person in 2026) and may require filing a gift tax return the year contributions are made. However, most experts expect Congress to fix this drafting oversight, but it hasn't happened yet. We are monitoring it closely.

Update (7/8/26): The IRS issued Revenue Procedure 2026-25, resolving the gift tax issue above. As long as contributions are cash, the child is under 18, and your total gifts to that child for the year — including the Trump Account contribution — stay under $19,000, contributions now qualify for the annual gift tax exclusion and don't require filing a gift tax return (Form 709).

The catch? It's all-or-nothing. Go over $19,000 in total gifts to that child (Trump Account contribution + anything else), and all your contributions to that child lose the exclusion and must be reported on Form 709.

- Full access at 18

At 18, your child has complete, unrestricted control over the account. They can withdraw everything immediately. While it will be subject to income tax and a 10% early withdrawal penalty, that may not stop a determined 18-year-old. Compare this to a 529 plan, which has rules around how the money is used, whereas this account does not. - State taxes may still apply

Some states do not conform to the federal tax treatment, meaning growth inside the account could be taxed annually at the state level. Whether this erodes the benefit depends on where you live. And, while some States allow you to deduct contributions to 529 Plans, there will be no income tax deduction for contributions made to a Trump Account. - It grows as a traditional IRA, not as a Roth

Withdrawals in retirement in excess of after-tax contributions are taxed as ordinary income, and required minimum distributions kick in at age 75. A Roth conversion at age 18 (when the child likely has low income) can address this, but it requires planning and has a potential "kiddie tax" timing wrinkle if the child is still claimed as a dependent.

How Do Trump Accounts Compare to 529 Plans?

529 plans have been a staple in financial planning and education planning, but now that Trump Accounts are here, what are the differences between them?

| Feature | Trump Account | 529 Plan |

|---|---|---|

| Annual contribution limit | $5,000 | Unlimited (gift tax rules and state limits apply) |

| Requires earned income | No | No |

| Tax treatment | Tax-deferred growth; taxed on withdrawal | Tax-free if used for education |

| Investment flexibility | Index funds only (until age 18) | Broad menu |

| Parental control after 18 | None – the child has full control | Yes, parent remains owner |

| Free government money | $1,000 (born 2025–2028) | No |

| Use restrictions | None after 18; standard IRA rules apply | Education (or limited Roth rollover) |

The Bottom Line

Trump Accounts are a new type of savings tool, and the confirmed details from the IRS are enough to act on for eligible families. The $1,000 pilot contribution is real, straightforward to claim, and worth pursuing. Employer contributions are equally clear-cut.

Where we encourage patience is around personal contributions. Several important questions (including gift and estate tax treatment, state-level conformity, availability of alternative custodians to Robinhood, and the long-term planning implications of the traditional IRA structure) do not yet have definitive answers. We will continue providing updates as guidance develops.

Our general advice would be to open an account for any eligible child to capture the government seed funds, as well as explore any employer contributions available to you. From there, we can help you determine whether your own contributions make sense for your specific situation.

Please consult with an attorney or a tax or financial advisor regarding your specific legal, tax, estate planning, or financial situation. The information in this article is not intended as legal or tax advice.